The European Central Bank (ECB) continues to reaffirm the most aggressive tightening cycle of its history in an effort to curb inflation. After a hike of 50 basis points (bps) on its February 2 meeting, the monetary institution has so far accumulated an increase of 300 bps since July 2022, bringing the deposit rate to 2.5%, coming from a territory of negative interest rates.

The last decision was fully expected by markets and the ECB further telegraphed its next move. In its statement, the Governing Council of the ECB was explicit in that it intends to raise interest rates by another 50 bps at the next monetary policy meeting in March, and “will then evaluate the subsequent path of its monetary policy.” The Council informed that decisions will be data dependent and follow a meeting-by-meeting approach after the next meeting.

In addition to policy rate increases, the ECB confirmed plans for a gradual reduction of its balance sheet, that was greatly expanded during the Covid-19 pandemic. This process, so called “quantitative tightening,” will take place from the beginning of March and is likely to last for several years as the Eurosystem will not reinvest all of the principal payments from maturing securities that were purchased under the asset purchase program (APP). The process will add another factor contributing to tightening credit markets.

In our view, the ECB will go through with the 50 bps hike scheduled for March and will hike another 25 bps in May, before pausing for evaluation. Three factors sustain our view.

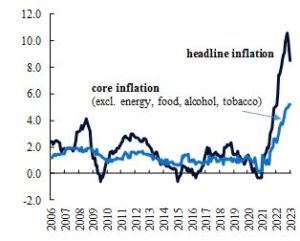

The argument in favour of additional rate hikes is that despite the recent improvement in headline inflation due to a significant moderation in gas prices, inflation is still too high. The latest data release came in with an increase of 8.5% year-on-year in January, below the 8.9% expected by analysts pooled by the Bloomberg consensus. This is still far above the 2% ECB target. Importantly, the measure of underlying inflation that excludes volatile items, such as energy and food prices, was at an all time high of 5.2%. In this context, another 75 bps of hiking is justified to further tighten financial conditions and prevent prices from de-anchoring.

Euro Area Inflation

(% year on year)

Source: Eurostat, QNB analysis

On the other hand, despite the recent positive surprises with Euro area activity data, indicating that a recession could potentially be avoided, the economy is still slowing. Market growth forecasts suggest that GDP could be stagnant in 2023. Hence, the ECB should remain cautious about overtightening when the economy is struggling. It is a difficult balance to achieve but, after rate increases in March and May, this should favour a pause to see how both the economy and core inflation are reacting to the new interest rate environment.

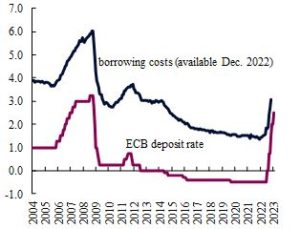

Key Euro Area Interest Rates

(% per year)

Source: ECB, QNB analysis

Finally, the traditional lags between interest rate hikes and their effects on the overall economy are particularly long in the Euro area, requiring additional prudence from policy makers. The unprecedented sequence of rate hikes has already translated into higher borrowing costs for firms. This will start weighing on investment this year, while the effects will take time to materialize fully. Firms in Europe are highly dependent on bank credit and a smaller proportion of their debt is issued through markets, which contrasts to the U.S. corporate sector that is overall relatively more reliant on debt markets. The pass-through of changes in monetary policy rates to bank lending interest rates is typically slower, implying that the full effects of the tightening cycle on credit conditions remain to be completed as monetary policy can take over 5 quarters to be felt completely for corporates and households. Furthermore, the costs of borrowing have increased for households, which will have an effect this year on housing investment and consumption. Longer lags mean more uncertainty about the impact of policy actions, which, in a period of high economic and inflation volatility, justify a pause in the aggressive policy tightening cycle for further assessment.

All in all, we expect another rate hike of 50 bps in March and a final increase of 25 bps in May, before the ECB settles the deposit rate at 3.25%. This is justified by much above target inflation rates. However, after May, the ECB should then pause for breath as the economy is still stagnant and the effects from the existing and incoming policy hikes have long lags that would play a part in affecting the economy only later this year and early next year, increasing the uncertain outcome.

What's happening in Tunisia?

Subscribe to our Youtube channel for updates.