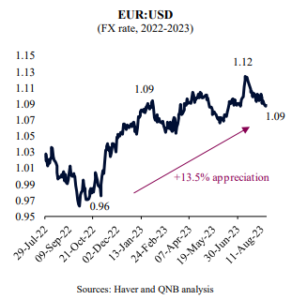

The Euro (EUR) has appreciated significantly against the US Dollar (USD) since September 2022, when it bottomed on the back of concerns about winter energy disruptions related to the Russo-Ukrainian conflict. The rally was supported by a relatively mild winter, the lower than expected decline in supply of energy and emergency fiscal support to corporates and households.

However, a more resilient US economy with a powerful re-accelerating dynamics are pointing to some USD strength more recently. Therefore, a year since the EUR rally begun, the Euro area currency is starting to show some signs of weakness, down 2.7% from the June 2023 peak. What can we expect from the EUR going forward?

The prevalent market view is that the EUR should be well supported by a natural adjustment from USD overvaluation and an European Central Bank (ECB) that is set to be more “hawkish” on interest rate policy than its peers in the US or Japan. In fact, markets are currently pricing a 1.8% appreciation of the EUR against the USD over the next 12 months to a EUR/USD rate of 1.12.

In our view, however, we expect a short-term USD rally that could take the EUR/USD back to the 1.05 levels over the next six months, before stabilizing around the 1.07-1.09 range in Q2-Q3 2024. Three arguments support our view, as we keep in mind that over the short-term or on a cyclical horizon, FX movements are dominated by changes in expectations for growth and real interest rate differentials, as well as the risk premium for geopolitical risks.

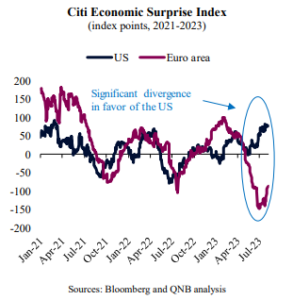

First, a flurry of negative economic data surprises in the Euro area versus positive surprises in the US suggest that expectations for growth differentials between the two economies will soon be significantly revised in favour of the US. This is reflected by a wide gap in the Citi Economic Surprise Index. In the US, high frequency estimators of growth suggest a GDP expansion of 5.8% annualized in Q3 2023, almost three times most estimates of trend growth. In contrast, the same type of indicators suggest a contraction in the Euro area for the same period. As a result, the growth gap is expected to further widen over the next couple of months.

Second, an overheated US economy amid above target inflation is likely to make the US Federal Reserve more “hawkish” than currently expected by the market. Importantly, the positive US economic momentum is set to gain further steam as forward looking indicators, such as the manufacturing Purchasing Managers’ Index (PMI) new orders-to-inventory ratio, point to a recovery of the currently weak US manufacturing as well. This would add to an economy that is already benefiting from low unemployment rates, fast wage growth, strong household consumption and robust service activity. In contrast, the ECB may have to pivot to a more “dovish” stance sooner than previously anticipated. This would favour a change in interest rate expectations that would favour the USD, as higher US yields would “pull” more European capital towards the US.

Third, geopolitical risks (Russo-Ukrainian conflict) are likely to rise over the next six months ahead of the European winter and the US pre-election cycle, favouring safe-haven demand for the USD. A plethora of high political, geopolitical and other tail risks could converge over the next few months, increasing the risk premium at the same time that it supports USD demand.

All in all, we expect to see USD strength over the short-term against the EUR, with the Euro area currency reversing more of the gains registered over the last 12 months. This is expected to be driven by a wider US-Euro area growth gap, wider interest rate differentials and more negative geopolitical trends.

What's happening in Tunisia?

Subscribe to our Youtube channel for updates.