Subdued global economic growth last year raised questions about the overall health of the Chinese economy. The country was for decades the main global growth engine. In fact, from the Great Financial Crisis of 2007-09 onwards, China was responsible for around 40% of total global economic expansion. Every year over the last several years, China’s growth added to the systeman amount equal to the total GDP of one of the major G-20 economy.

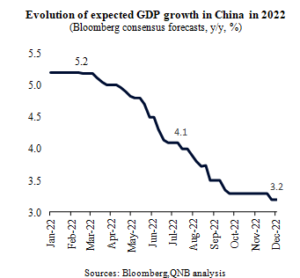

However, over the last several quarters, different domestic factors led to an overall economic slowdown in China. This was driven by the Zero Covid policy with lockdowns across major cities, restrictive bank lending to the overleveraged real estate sector and aggressive regulatory clampdowns on technology-related sectors. As a result, China’s expected growth plummeted throughout 2022.

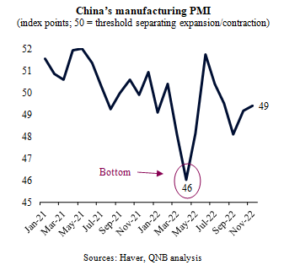

Despite the negative momentum, there are early signs that the Chinese economy may be about to turn a corner into a recovery mode. The Manufacturing Purchasing Managers’ Index (PMI) of China, a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, seemingly bottomed in April 2022.China’s manufacturing PMI is still below 50 index points, the threshold that traditionally separates contractionary from expansionary changes in business conditions, but it started to accelerate in recent months, despite new waves of Covid-19 cases.

In our view, however, four key policy pivots are set to spur a powerful cyclical recovery in China over the coming months.

First, China is rapidly pivoting away from Zero Covid policies, i.e., lockdowns and ultra-tight social distancing measures that aim to supress waves of new virus cases. This is being supported by the development of new Chinese mRNA vaccines as well as the availability of efficient antiviral pills.The recent decision of the State Council to flexibilize quarantine requirements and to urge elderly citizens to get vaccinated and even get boosted more often further reinforced this policy shift. Hence, a more stable “re-opening” should be secured, allowing economic activity to gain momentum.

Second, China is also pivotingits macroeconomic policy stance from neutral to supportive or accommodative. Chinese policymakers are becoming more concerned about the domestic economic slowdown and are starting to ease more aggressively. Policy actions so far include a few rounds of interest rate reduction, liquidity injections and fiscal spending in infrastructure projects. This supports aggregate demand andoverall economic activity.

Third, Chinese policymakers started to pivot from promoting a sharp de-leveraging of major property developers. Tighter credit conditions to real estate projects were causing sectoral debt distress, threatening the broader domestic financial system. In November 2022, regulators issued a comprehensive plan to boost the real estate sector.The plan included both a significant liberalization of property ownership in certain cities and financial support measures to developers facing liquidity problems. This should enhance confidence in the sector and allow for more investments.

Forth, Chinese authorities are pivoting away from open-ended regulatory changes in key technological sectors. Over the last several quarters, comprehensive regulatory reviews in certain industries, such as private education, fin-tech, e-commerce, food delivery and ride hailing, created severe business uncertainty, partially preventing new investments and even innovation in related activities. In recent months, however,authorities started toconclude their regulatory reviews, providing clearer guidance for businesses and issuing more formal licenses to operate to important corporates that were previously operating under “grey areas.”This is lessening business uncertainty and should start supporting private sector investments and innovation.

All in all, major policy changes in healthcare, real estate and business regulation should further boost the Chinese cyclical recovery, promoting above consensus growth in 2023. In fact, while consensus forecasts point to 4.9% growth in China this year, we expect to see a GDP expansion of 5.5% for the same period.

What's happening in Tunisia?

Subscribe to our Youtube channel for updates.